by Amy Irvine

November was National Caregiver Month and this year for the Irvine household, this was especially meaningful.

Many of you know that this past summer, Brent, and his brothers, took on the role of full-time caregiver for his mom. Eva had dementia, but we were lucky, as it really just affected her short-term memory. She would repeat herself and hyper focus on a topic sometimes, but she was sharp on what happened years ago and she always recognized everyone in the family. She also still held her witty personality.

As she aged, she made it VERY clear to us all that she did not want to go into a nursing home, and we didn’t want her to have to live in one either. Especially in COVID times. So we made every effort we possibly could to keep her home.

She would look you square in the eye and say, “DON’T PUT ME IN A DAMN NURSING HOME!!!” If you didn’t know her, it sounded like a demand, but it was really a plea. You see, she witnessed her mom and a couple of sisters living in a nursing home and she did not want that experience. This was a case of being afraid of the known, not the unknown.

I’m sharing this with you all now because many of you are “at that age” in life where you may also find yourself in this situation. It sounds easy, many cultures take care of their elders, but in our culture where most households need two incomes and don’t live with their parents (or even in the same State as their parents), it is both an emotional and a financial decision to take care of an aging family member.

Emotional Side

Most of the time it is a slow transition. You start to notice small things and increase your “check in” visits. But when you see hygiene and eating habits start to slide, your concern starts to increase.

Then, as you have the dreaded “you shouldn’t be driving” conversation (what we call the “other talk”), not only is that emotional to the person receiving the news, but it is extremely hard for the caregiver giving the news. YOU have just removed their independence in lieu of their safety, but often they only realize the loss of independence.

Once you do move into full caregiving mode, the fact that you have now become “the parent” to your parent(s) is not an easy pill to swallow. It’s one thing to bathe your children, it’s a whole different set of emotions when you have to bathe your parent(s).

One afternoon as I sat with Eva, I watched her napping. For whatever reason, I thought of the journey of life. Had she been a sleeping child, peacefully breathing in and out, it would have brought such joy. But to sit and watch that very same action, in a labored manner, brought such sorrow. The same action - a very different emotion.

Financial Side

Brent and I knew what we were going to do, but we didn’t go into it blindly. We knew it was going to mean that his income was going to go to zero.

But it wasn’t just his income we would be forgoing, we knew that we were going to have to adjust our lifestyle so that we could continue with his retirement savings and some of our other savings goals. This wasn’t as hard for us because we really couldn’t get away to do that much and we were limiting our exposure to others to make sure we didn’t compromise her health situation further. But for many others, in order to pay their bills, they will need to give up saving for retirement, for travel, for college, and for other goals. They may need to take into consideration their own health insurance coverage, loss of life and disability insurance through their employer, and all of the other benefits that they may be walking away from to take on this role.

Many may be able to take family leave and continue with the benefits, but you don’t necessarily know how long you are going to need to be on leave and you need to explore what benefits will continue.

You also should do the math on what you need to do to make up for the financial impact after the fact. Will you need to put more away in your retirement accounts, health care accounts, college funding, etc. once you return to your job? What is the math behind the situation?

Also, be aware of what your parents might have for a long-term care policy; some will allow money to be used for any caregiving (including family) and some will limit to agency care. If your parents decided to self fund their care, you may want to consider hiring someone to come in several days a week to allow you to get a break. In our experience, this was easier said than done, but we were lucky enough to find a wonderful young woman to assist us several days a week for a few hours at a time.

I would strongly recommend that you do some research in advance if you feel your parents might need some assistance in the future. Have a list of contacts, do some interviews, and be prepared to start slowly integrating them into your parents lives. This is both emotional and financial in nature, and should be planned for in advance.

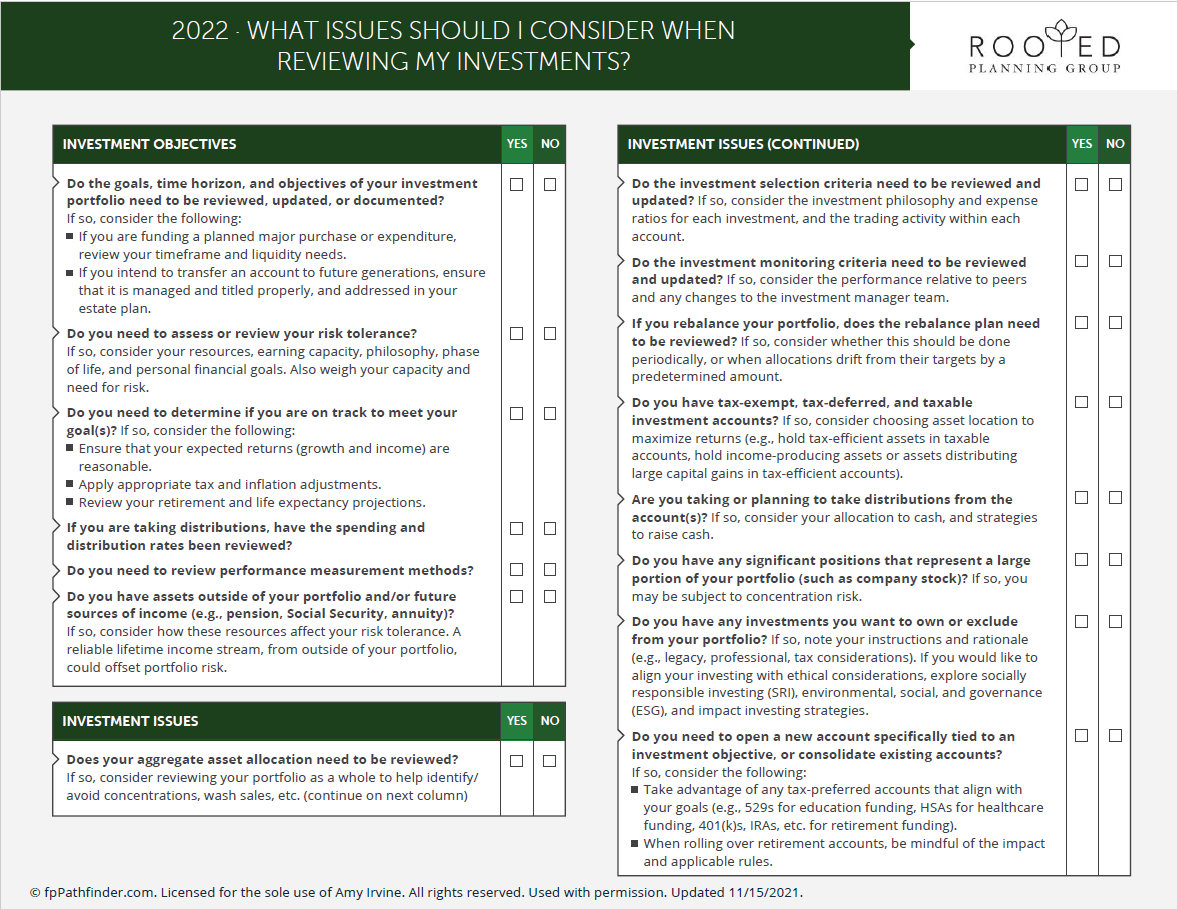

How to Plan for Your Future Aging-Self

In the conversations I have with our clients, I point blank ask them - what do you want, after all no one wakes up one day and says, I’d like to move into a nursing home today?

Do you want at home care? Are you willing to let someone outside your family come in? Have we planned for that cost?

Do you prefer to move to a continuing care facility - where you start out living independently, but more care is provided as you need it? Have you planned for that cost?

What role do you want your family to plan in your caregiving? What does that mean for them?